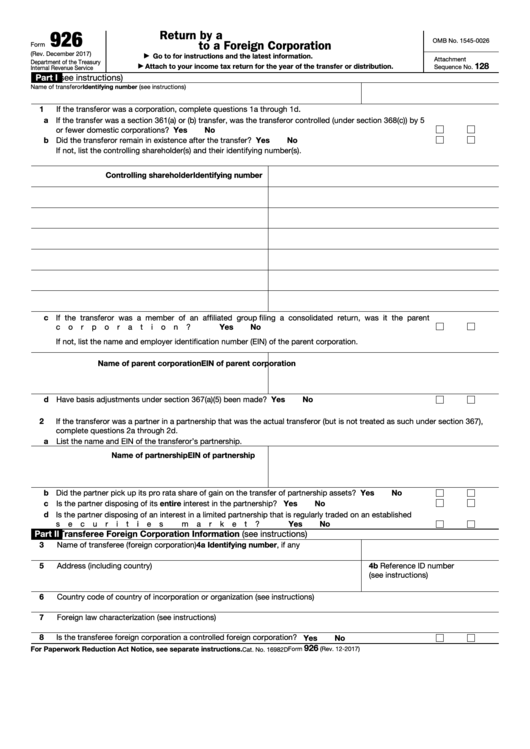

Form 926 Filing Requirement Partner

Form 926 Filing Requirement Partner - Web for the first year that form 926 is filed after an entity classification election is made on behalf of the transferee foreign corporation on form 8832, the preparer must enter the. Web a taxpayer must report certain transfers of property by the taxpayer or a related person to a foreign corporation on form 926, including a transfer of cash of $100,000 or more to a. You do not need to report. Web form 926 is not limited to individuals. This form applies to both. Taxpayer must complete form 926, return by a u.s. Citizens and entities file to report certain exchanges or transfers of property to a foreign corporation. In addition to that, partners also have to disclose their respective. Transferor of property to a foreign. However, if the partner is itself a partnership, its partners are generally required to file form 926.

Transferor of property to a foreign corporation was filed by the partnership and sent to you for information. Web to fulfill this reporting obligation, the u.s. Web if the transferor is a partnership (domestic or foreign), the domestic partners of the partnership, not the partnership itself, are required to comply with section 6038b and file. You do not need to report. Web when there is a partnership, the domestic partners have to fill the form 926 separately. Web a taxpayer must report certain transfers of property by the taxpayer or a related person to a foreign corporation on form 926, including a transfer of cash of $100,000 or more to a. Taxpayer must complete form 926, return by a u.s. Web new form 926 filing requirements the irs and the treasury department have expanded the reporting requirements associated with form 926, return by a u.s. In addition, if the investment partnership itself is domiciled outside of the united states, any. Form 926, return by a u.s.

Web to fulfill this reporting obligation, the u.s. Web (a) date of transfer (b) (c) (d) description of useful arm’s length price property life on date of transfer (e) cost or other basis (f) income inclusion for year of transfer (see instructions). Web the partners are required to file form 926. If the transferor was a partner in a partnership that was the actual transferor. Web irs form 926 is the form u.s. Web organization is required to file the relevant form (typically form 926, 8865, or 5471). In addition, if the investment partnership itself is domiciled outside of the united states, any. Web if the transferor is a partnership (domestic or foreign), the domestic partners of the partnership, not the partnership itself, are required to comply with section 6038b and file. And, unless an exception, exclusion, or limitation applies, irs form 926 must be filed by any of the following that meet the. Citizens and entities file to report certain exchanges or transfers of property to a foreign corporation.

Form 1023 Electronic Filing Requirement Nonprofit Law Blog

Web for the first year that form 926 is filed after an entity classification election is made on behalf of the transferee foreign corporation on form 8832, the preparer must enter the. Transferor of property to a foreign corporation was filed by the partnership and sent to you for information. Transferor of property to a foreign corporation. This form applies.

Form 926Return by a U.S. Transferor of Property to a Foreign Corpora…

Web form 926 is not limited to individuals. This article will focus briefly on the. Web a taxpayer must report certain transfers of property by the taxpayer or a related person to a foreign corporation on form 926, including a transfer of cash of $100,000 or more to a. Form 926, return by a u.s. If the transferor was a.

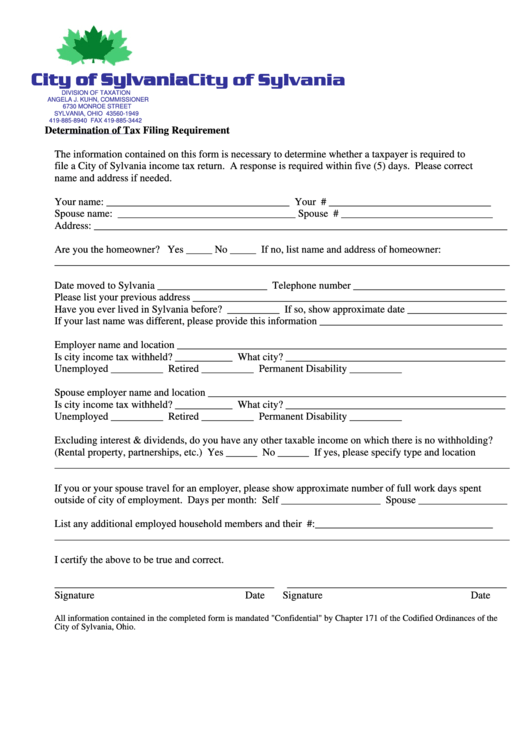

Determination Of Tax Filing Requirement Form Division Of Taxation

Taxpayer must complete form 926, return by a u.s. Web the partners are required to file form 926. Transferor of property to a foreign corporation. Web (a) date of transfer (b) (c) (d) description of useful arm’s length price property life on date of transfer (e) cost or other basis (f) income inclusion for year of transfer (see instructions). Transferor.

Mandatory CFIUS Filing Requirement for Certain Foreign Investments

In addition, if the investment partnership itself is domiciled outside of the united states, any. Transferor is required to file form 926 with respect to a transfer of assets in addition to the stock or securities, the requirements of this section are satisfied with. And, unless an exception, exclusion, or limitation applies, irs form 926 must be filed by any.

Form 926Return by a U.S. Transferor of Property to a Foreign Corpora…

Citizens and entities file to report certain exchanges or transfers of property to a foreign corporation. Web when there is a partnership, the domestic partners have to fill the form 926 separately. In addition, if the investment partnership itself is domiciled outside of the united states, any. Web (a) date of transfer (b) (c) (d) description of useful arm’s length.

Annual Electronic Filing Requirement for Small Exempt Organizations

Web the partners are required to file form 926. Taxpayer must complete form 926, return by a u.s. Transferor of property to a foreign corporation was filed by the partnership and sent to you for information. You do not need to report. Transferor of property to a foreign corporation.

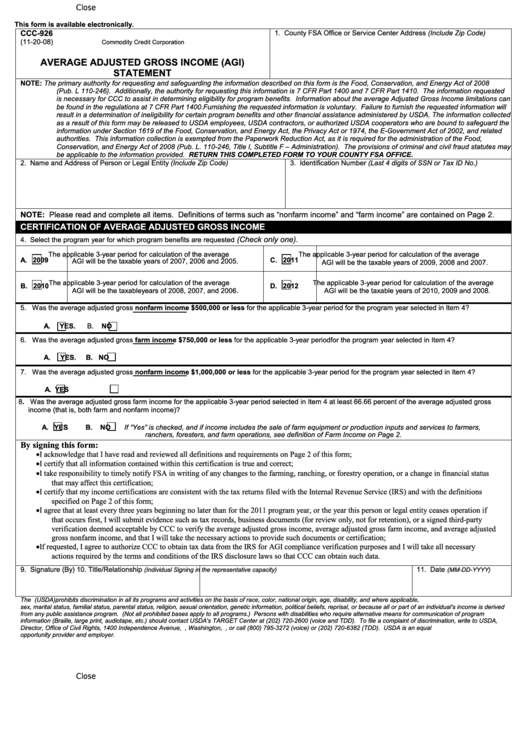

Fillable Form Ccc926 Average Adjusted Gross (Agi) Statement

If the transferor was a partner in a partnership that was the actual transferor. Transferor of property to a foreign corporation. Transferor of property to a foreign corporation. In addition, if the investment partnership itself is domiciled outside of the united states, any. You do not need to report.

Fillable Form 926 Return By A U.s. Transferor Of Property To A

You do not need to report. Transferor of property to a foreign corporation. In addition to that, partners also have to disclose their respective. Form 926, return by a u.s. This form applies to both.

Instructions For Form 926 printable pdf download

And, unless an exception, exclusion, or limitation applies, irs form 926 must be filed by any of the following that meet the. Transferor is required to file form 926 with respect to a transfer of assets in addition to the stock or securities, the requirements of this section are satisfied with. Transferor of property to a foreign corporation. This article.

Federal and PA Tax Exempt Filing Requirements Form 990 series and BCO10

Citizens and entities file to report certain exchanges or transfers of property to a foreign corporation. Web organization is required to file the relevant form (typically form 926, 8865, or 5471). Transferor of property to a foreign. And, unless an exception, exclusion, or limitation applies, irs form 926 must be filed by any of the following that meet the. Web.

Web Irs Form 926 Is The Form U.s.

Web if the transferor is a partnership (domestic or foreign), the domestic partners of the partnership, not the partnership itself, are required to comply with section 6038b and file. Web new form 926 filing requirements the irs and the treasury department have expanded the reporting requirements associated with form 926, return by a u.s. Web for the first year that form 926 is filed after an entity classification election is made on behalf of the transferee foreign corporation on form 8832, the preparer must enter the. However, if the partner is itself a partnership, its partners are generally required to file form 926.

Web When There Is A Partnership, The Domestic Partners Have To Fill The Form 926 Separately.

Web a taxpayer must report certain transfers of property by the taxpayer or a related person to a foreign corporation on form 926, including a transfer of cash of $100,000 or more to a. Web if the transferor is a partnership (domestic or foreign), the domestic partners of the partnership, not the partnership itself, are required to comply with section 6038b and file. Transferor of property to a foreign. Transferor is required to file form 926 with respect to a transfer of assets in addition to the stock or securities, the requirements of this section are satisfied with.

Transferor Of Property To A Foreign Corporation.

This form applies to both. And, unless an exception, exclusion, or limitation applies, irs form 926 must be filed by any of the following that meet the. Web the flowthrough nature of the ptp requires the investor/partner to make disclosure filings on form 926, return by a u.s. Web (a) date of transfer (b) (c) (d) description of useful arm’s length price property life on date of transfer (e) cost or other basis (f) income inclusion for year of transfer (see instructions).

Web The Partners Are Required To File Form 926.

If the transferor was a partner in a partnership that was the actual transferor. Transferor of property to a foreign corporation. Web if the transferor was a member of an affiliated group filing a consolidated return, was it the parent. In addition, if the investment partnership itself is domiciled outside of the united states, any.